In the metabolism of retirement planning, we treat market crashes as acute injuries. But a long-term care event is a chronic inflammation that slowly—and then suddenly—dissolves a portfolio’s principal. For many families in Erie and Boulder, the cost of care in 2026 has crossed a threshold where "hope" is no longer a viable strategy.

The metabolic shift: Moving from the "Trap" of traditional LTC to the "Leverage" of Asset Care.

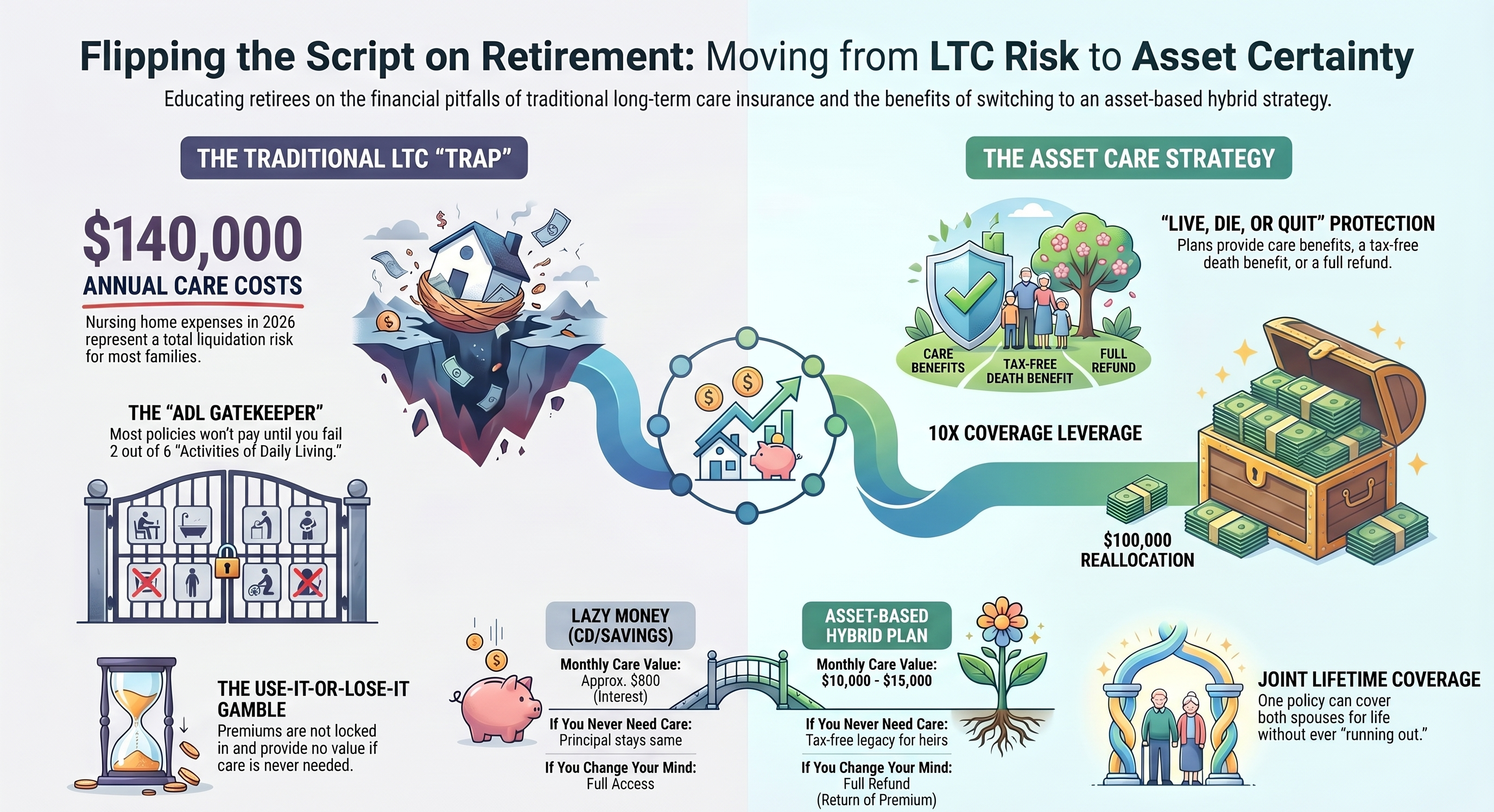

The 2026 Reality Check:

Annual nursing home costs are averaging $140,000. For a couple, a three-year care event could represent a $420,000+ liquidation event, often occurring at the exact moment the market is down or taxes are up.

The "ADL Gatekeeper" and the Traditional Trap

Traditional Long-Term Care (LTC) insurance was built on a "use-it-or-lose-it" model. It operates much like car insurance: you pay a premium, and if you never crash, the money is gone. However, the The Care Paradox lies in the gatekeeping mechanics.

Most traditional policies will not trigger benefits until you fail 2 out of 6 "Activities of Daily Living" (ADLs). This creates a massive gap where families need significant help—memory care, home assistance, or specialized therapy—but don't yet "qualify" in the eyes of the carrier. You are left paying premiums while simultaneously paying out-of-pocket for care.

The Erosion of Premium Certainty

Unlike your mortgage or a fixed annuity, traditional LTC premiums are not locked in. Carriers can, and frequently do, petition the state to raise rates on existing policyholders. We have seen retirees forced to choose between a 50% rate hike or letting a policy lapse after paying into it for 20 years. This is the ultimate "Gamble" highlighted in the infographic: paying for protection that may become unaffordable exactly when you need it most.

Reallocating "Lazy Money" for 10X Leverage

At Flatirons, we look at the Mathematics of Reallocation. Many retirees keep "Lazy Money" in CDs or savings accounts as an emergency fund. While safe, this money has low metabolic efficiency—it only grows at 4-5% interest.

By moving a portion of that stagnant principal (e.g., a $100,000 reallocation) into an Asset-Based Hybrid Plan, we transform that asset:

- 10X Coverage: That same $100,000 can provide $10,000–$15,000 in monthly care value.

- Joint Lifetime Coverage: Modern strategies can cover both spouses under one policy, ensuring the first spouse's care doesn't leave the second spouse penniless.

- The "Quit" Option: Unlike traditional insurance, if you change your mind, many hybrid plans offer a full Return of Premium. You keep your principal.

The "Live, Die, or Quit" Philosophy

Systemic retirement planning requires Asset Certainty. You should never pay for a benefit that doesn't provide value regardless of the outcome. With a hybrid strategy:

- LIVE: You have a massive tax-free pool for care.

- DIE: Your heirs receive a tax-free death benefit if you never need the care.

- QUIT: You can walk away with your original principal (Return of Premium).

Protect Your Metabolic Engine

Are you relying on "Lazy Money" to cover a $140,000/year risk? Let's run a stress test to see how your portfolio would handle a care event today.