The 2.8% Illusion

Strategic Analysis: Purchasing Power & Medicare Friction

Matthew J. Welt, RSSA®

Registered Social Security Analyst®

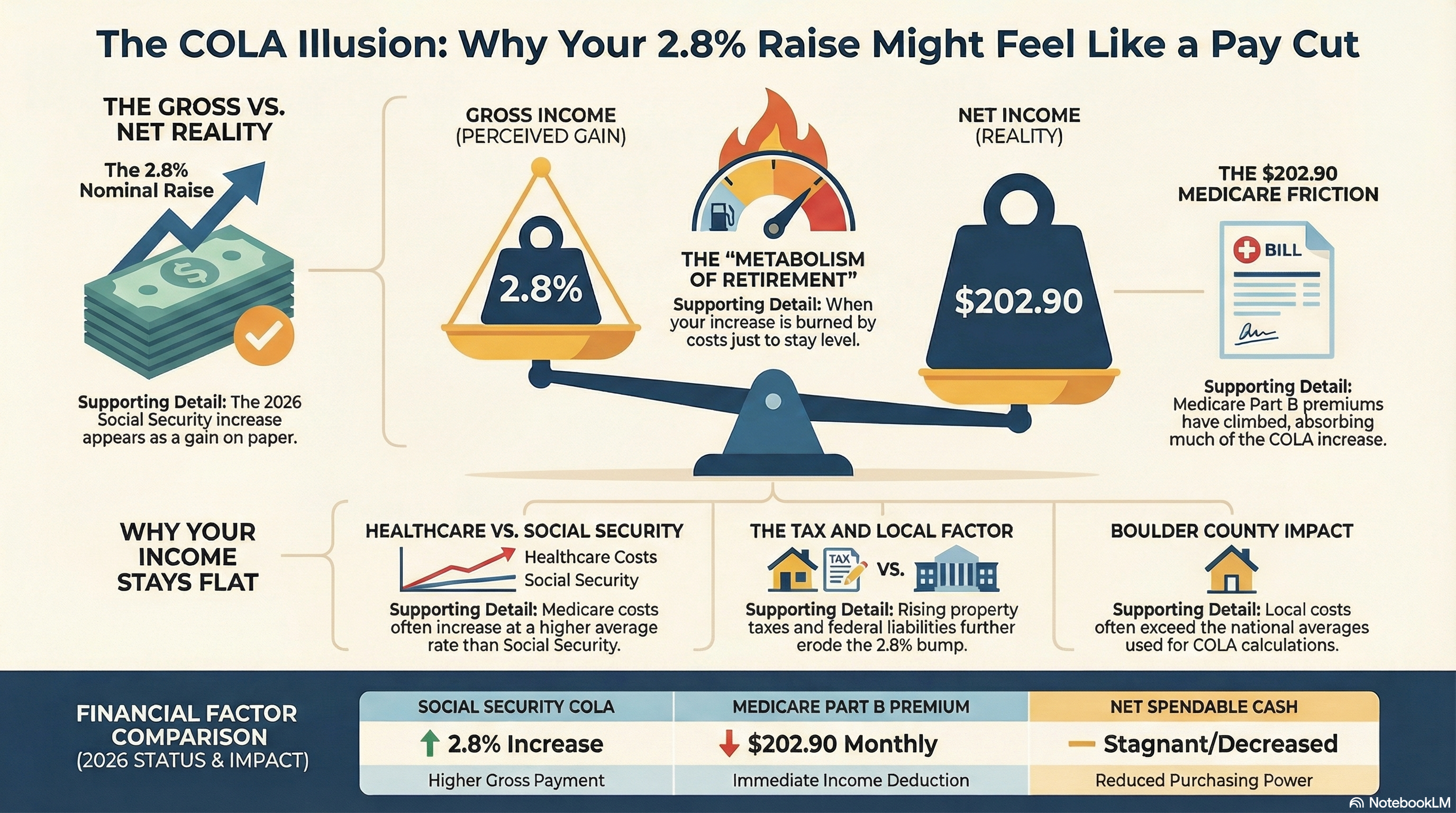

The headlines in early 2026 were clear: a 2.8% Cost-of-Living Adjustment (COLA) for Social Security recipients. For many, this appeared to be a necessary boost in a post-inflationary world. However, at Flatirons Retirement, we look deeper than the headline percentage.

1. The Concept of Financial Friction

In my framework, the Metabolism of Retirement, we evaluate how efficiently your wealth converts into usable, lifestyle-sustaining income. Just like biological metabolism can be slowed by external stressors, your financial metabolism is slowed by "friction."

In 2026, the primary friction point is the Medicare Part B Premium. For many recipients, the standard premium has risen to $202.90 per month. When you subtract the increased Medicare deduction from the 2.8% COLA raise, the "net" increase is often negligible. If your expenses (housing, fuel, and food here in Colorado) are rising faster than that net increase, you are experiencing a Purchasing Power Deficit.

"Real retirement security isn't found in the gross dollar amount the government sends you; it's found in the net efficiency of that dollar after it survives the gauntlet of taxes and premiums."

2. The "Front Range" Reality

The federal government uses the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) to calculate these raises. This is a broad, national average that includes everything from the cost of milk in Kansas to the price of rent in Florida.

It does not, however, account for the unique economic pressures we face in Erie, Boulder, and the surrounding Front Range. Local property tax assessments and the rising cost of services in our specific corridor often outpace the national average. When a 2.8% federal "raise" meets a 5% local cost increase, your retirement metabolism enters a catabolic state—where it begins to "eat itself" by forcing you to dip into principal assets earlier than planned.

3. The RSSA® Strategy: Optimization Over Observation

As a Registered Social Security Analyst, my role is to help you move from being a passive observer of government adjustments to an active optimizer of your benefits. The 2.8% Illusion proves that Social Security, while a foundation, cannot be your only defense against inflation.

We solve this through Volatility Buffers. By integrating life insurance cash values or specific annuity structures, we create a "swing fund." When the COLA is low and inflation is high, we draw from the buffer to protect your standard of living, allowing your primary investments time to recover.

Conclusion: Re-Calibrating Your Plan

The 2026 COLA update is a wake-up call. It highlights the friction inherent in the system and the need for a more metabolic approach to wealth management. We don't just want your money to last; we want your spending power to stay robust regardless of what the federal government decides the cost of living "should" be.

Take the Next Step

If you are concerned that your current strategy isn't keeping pace with the real-world costs of the Front Range, let's conduct a Systemic Audit of your filing plan.

Schedule Audit