The Rockefeller Strategy: Building Generational Opportunity Without Creating Entitlement

Matthew J. Welt, RSSA®

Registered Social Security Analyst®

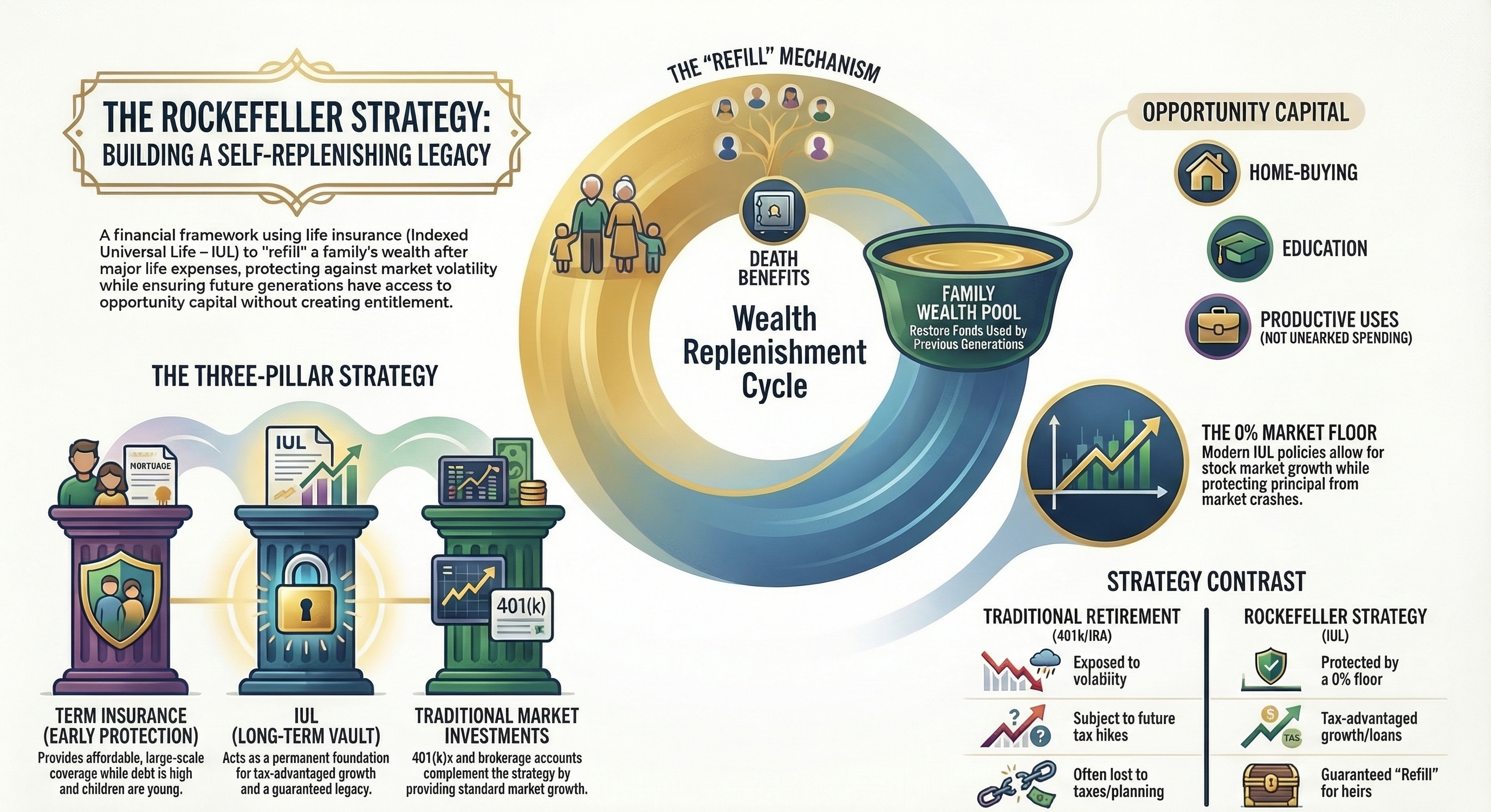

The Rockefeller Strategy is a financial method used by some of America’s wealthiest families to protect and pass down wealth. Instead of letting money disappear through spending, taxes, and market drops, these families use life insurance as a replenishment system.

When the family uses money for investments or business needs, the life insurance death benefit eventually refills that capital for the next generation. While this was once done with traditional whole life insurance, many families now use Indexed Universal Life (IUL) because it offers more growth potential, lower costs, and tax-free access to cash.

The Problem Most Families Face

Most people work hard and save in 401(k)s or IRAs. These are good tools, but they often fall short in three areas:

- Volatility: Market crashes can shrink your savings right when you need them.

- Taxes: If tax rates go up, your future spending power goes down.

- Leakage: When money moves to the next generation, much of it can be lost to taxes or poor planning.

Standard retirement accounts don't always provide a guaranteed legacy or protection from market downturns. That is where a properly structured policy fills the gap.

What the Strategy Actually Does

The goal wasn't just to buy insurance; it was to build a foundation. The concept was simple: the policy created tax-advantaged growth, provided cash when the family needed it, and the death benefit restored the family's wealth every generation.

Crucially, the goal wasn't to create "unlimited wealth" for someone to live off forever. Instead, it created Opportunity Capital. This is enough money to help a grandchild go to college, buy a first home, or start a business, but not so much that they lose their drive to work. It’s designed to create opportunity, not entitlement.

Why Indexed Universal Life (IUL) Fits

Modern IUL policies offer several specific advantages for this strategy:

- Growth with a Safety Net: IULs grow based on stock market indexes (like the S&P 500). When the market goes up, you get upside potential. When the market drops, a 0% floor protects you from losing your principal.

- Lower Costs: When a policy is "max-funded" for cash growth rather than just a big death benefit, the internal fees are often lower, making the money grow more efficiently.

- Tax-Free Access: You can take loans or withdrawals from the policy, often tax-free. This provides "emergency" or "opportunity" money for retirement or business ventures without disrupting your other investments.

- Permanent Protection: Unlike term insurance that expires, an IUL lasts your whole life. The death benefit replenishes the assets you spent during retirement, "refilling the tank" for your heirs.

A Simpler Way to Handle Legacy

Many families think they need complex, expensive trusts to pass down wealth. A simpler way is to make a trust the owner and beneficiary of the life insurance policy itself. This lets the policy act as its own financial system. Instead of asking a bank for permission to use money, future generations can access capital through policy loans, which offers more flexibility and fewer legal hurdles.

Putting It All Together: A Practical Example

For most families, this strategy works best when three different tools are used together:

- Term Insurance: Provides large, affordable protection while you're raising a family.

- IUL: Acts as the long-term "vault" that builds cash and provides a permanent death benefit.

- Traditional Investments: Your 401(k) and brokerage accounts continue to grow with the market.

This combination gives you protection during your working years, tax-free income in retirement, and opportunity capital for your children and grandchildren.

Frequently Asked Questions

Is the Rockefeller Strategy only for the ultra-wealthy?

No. While it started with families like the Rockefellers, modern tools like IUL make it possible for everyday families to use the same principles. The goal isn't necessarily to become a billionaire; it's to provide financial opportunity for your children and grandchildren.

Why use an IUL instead of a traditional Whole Life policy?

Modern IUL policies often offer better growth potential because they are tied to market indexes like the S&P 500. They also tend to have lower costs and more flexibility in how you pay your premiums, making them a more efficient "engine" for accumulation.

How does life insurance create "generational wealth"?

It acts as a replenishment system. You can use the cash value during your life for retirement or big purchases. When you pass away, the tax-free death benefit refills that pot of money for your heirs, so the wealth doesn't just disappear after one generation.

What is the benefit of putting the policy in a trust?

Using a trust as the owner can simplify the handoff to the next generation. It allows the policy to function as its own financial system where heirs can access capital through policy loans without the heavy red tape or tax hurdles of a standard inheritance.

About Me: How I Help You Build This Plan

I specialize in taking these "elite" financial concepts and making them practical for the average family. I don't believe in one-size-fits-all plans; instead, I help you coordinate three specific "buckets" to ensure your strategy is solid:

- Immediate Protection: We use Term Insurance to provide a massive safety net while your kids are young and your mortgage is high.

- The Opportunity Vault: We set up a properly structured IUL to build cash value over time for tax-free retirement income or "opportunity capital."

- Market Growth: We keep your 401(k), IRAs, and brokerage accounts moving as your growth engines, with the IUL acting as the "buffer."

My goal is to help you build a legacy that provides opportunity without entitlement. I want your kids to have a head start, but I also want them to keep the same drive to succeed that you have today.