In the financial world, the debate over life insurance often feels like a heated sports rivalry. On one side, you have the "Buy Term and Invest the Difference" crowd. On the other, the "Permanent Cash Value is King" camp.

Most people feel like they have to pick a side. But the truth is, the smartest financial strategy isn’t about winning a debate—it’s about protecting your family today while building a vault for your future wealth. When you look at the **"Metabolism of Retirement,"** you realize that your needs change as you age. Here is why a balanced approach is usually the winning move.

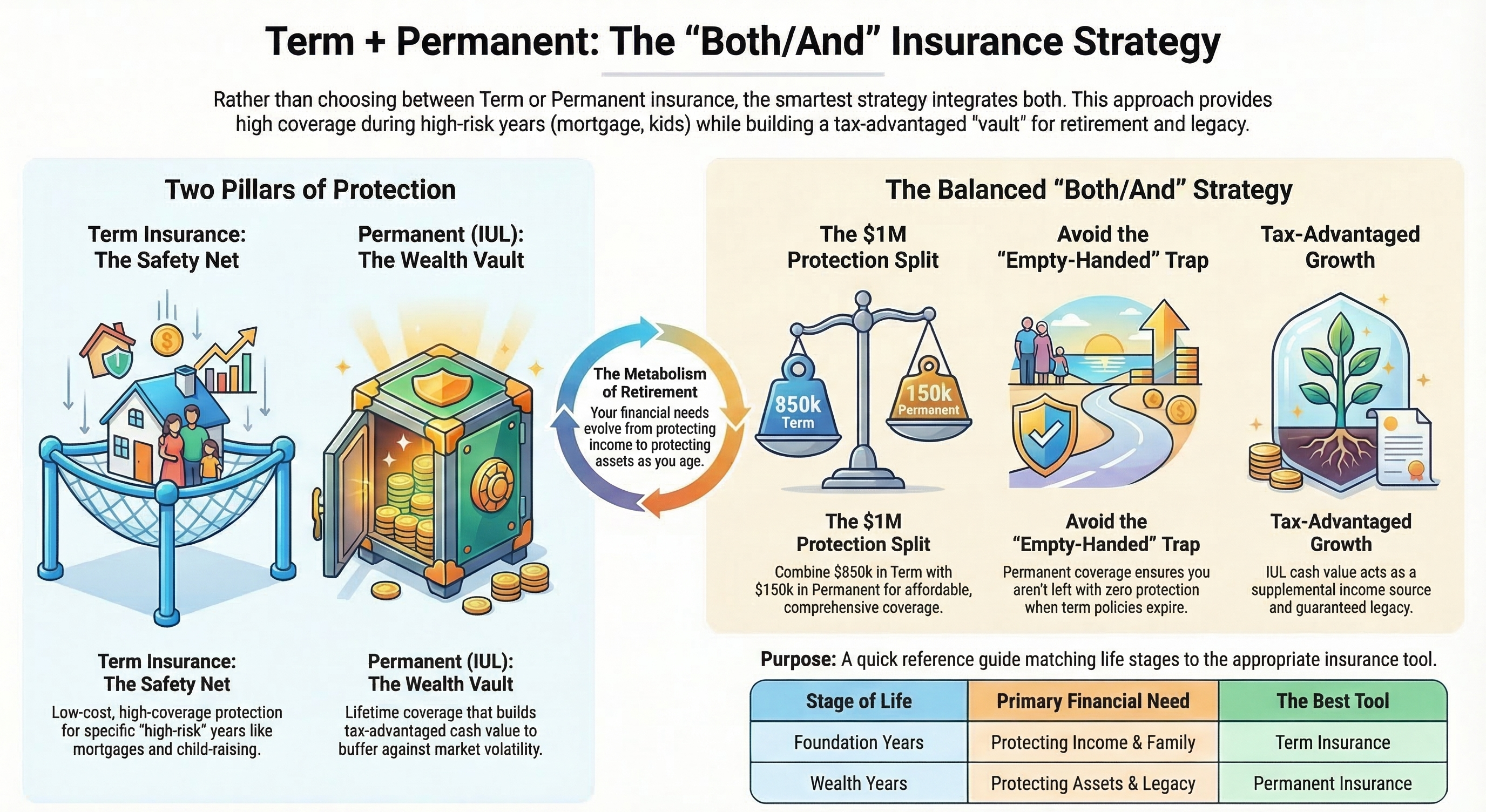

1. Term Insurance: Your "Safety Net" for the High-Risk Years

Term insurance is straightforward: you pay a low monthly premium for a large amount of coverage that lasts for a set period, like 20 or 30 years.

- The Goal: To protect your family during your most vulnerable "wealth-building" years—when you have a large mortgage, young children, and haven't yet reached your full savings potential.

- The Benefit: It is incredibly cost-effective. For example, a healthy 35-year-old can often secure $850,000 of coverage for around $100 a month.

- The Catch: It eventually expires. If you rely only on term insurance, you may find yourself at age 65 with zero protection just as you’ve finally accumulated significant wealth.

2. Permanent Insurance (IUL): Your "Vault" for Future Wealth

Indexed Universal Life (IUL) is permanent coverage designed to last your entire life while building "cash value" that you can access.

- The Goal: To protect your assets and leave a legacy after your high-risk years are over.

- The Benefit: Properly structured IULs act as a tax-advantaged asset. They can provide a supplemental income source in retirement, a "volatility buffer" during market downturns, and a guaranteed legacy for your heirs.

- The Catch: It is a larger commitment. Using only permanent insurance to cover a young family’s total needs could cost $500 or more per month, which might limit your ability to fund other investments like a Roth IRA.

Why a "Both/And" Strategy Wins

The most effective plans evolve as you do. By combining both types of insurance, you get the best of both worlds without breaking the budget.

The Balanced Approach in Action:

Imagine a 35-year-old who needs $1,000,000 in total protection. Instead of choosing one or the other, they structure it like this:

- $850,000 in Term Coverage: Low cost, high protection for the mortgage and child-raising years.

- $150,000 in Permanent (IUL) Coverage: Building tax-advantaged cash value for the long haul.

The Result: The family is fully protected for $1,000,000 today. When the term policy expires in 30 years, they still have a permanent death benefit and a significant "vault" of cash value to support their retirement strategy.

| Stage of Life | Primary Financial Need | The Best Tool |

|---|---|---|

| The Foundation Years | Protecting Income & Family | Term Insurance |

| The Wealth Years | Protecting Assets & Legacy | Permanent Insurance |

The Bottom Line

Life insurance isn’t just a "death benefit"—it’s a living tool to manage risk. Term insurance protects your foundation, while permanent insurance protects your future. By integrating both, you ensure that your family never has to rely on a fundraiser or a GoFundMe if the unexpected happens. Real financial planning is about providing peace of mind for every stage of your life's journey.